From a spot with no cellular signal and no tower for miles, an ordinary iPhone can now send a text message. It travels straight up to a satellite roughly 300 miles overhead — one moving at nearly five miles per second — and back down to Earth. For a century, "no signal" was effectively a fact of nature. It is becoming a temporary condition, and the companies racing to erase it are spending billions to do so.

The capability, known in the industry as direct-to-device, runs on hardware consumers already own — no dish and no special handset. That distinction is the whole story: satellite phones are not new, but making a standard phone reach orbit is a different problem, and it was widely considered impractical until recently.

Satellite phones used to be bricks

The last serious attempt at consumer satellite phones is a cautionary tale. In 1998, Motorola spent roughly $5 billion to launch Iridium, a constellation meant to let a phone work anywhere on Earth. The handset was the size of a brick, cost about $3,000, and billed between $6 and $30 a minute. The company filed for Chapter 11 bankruptcy in 1999, among the largest in US history at the time, and its assets were later sold for $25 million. The lesson, for two decades, was that satellites and ordinary phones did not mix.

Three approaches, one race

Today three distinct efforts are delivering the service commercially. Apple (NASDAQ: AAPL) has, since the iPhone 14, built satellite connectivity into every handset — first for emergency use and, since iOS 18, for standard text messages off the grid, using the Globalstar network. The feature is free for two years and now works across the US, Canada, Mexico, Japan and other countries.

T-Mobile (NASDAQ: TMUS), partnered with the privately held SpaceX, launched a commercial service called T-Satellite in July 2025 that uses more than 650 Starlink satellites as cell towers in orbit. It costs about $10 a month, works on AT&T (NYSE: T) and Verizon (NYSE: VZ) phones as well, and covers over 500,000 square miles of territory no ground tower reaches.

AST SpaceMobile (NASDAQ: ASTS) is pursuing the most extreme approach, flying the largest antennas ever launched. Its BlueBird 6 satellite unfolded an array of roughly 2,400 square feet — about the footprint of a small house, and the largest commercial communications antenna placed in low Earth orbit — with AT&T, Verizon, Vodafone and Google among its backers.

Why it should not work

The physics is unforgiving. A phone transmits about one watt, a whisper that must reach a satellite some 300 miles up. Closing that link is why AST builds antennas the size of a house: the receiver has to be enormous to hear a signal so faint. The satellite is also moving at about 7.5 kilometers per second, which smears the signal's frequency through the Doppler effect — a shift that can reach tens of kilohertz and changes every second it crosses the sky. To compensate, a phone uses its own GPS position and the satellite's known path to pre-correct its timing and frequency before transmitting, so the signal arrives already tuned.

The change was a paragraph, not a rocket

What allowed three companies to solve this at roughly the same time was not a hardware breakthrough but a standard. In 2022, 3GPP — the body that writes global 4G and 5G specifications — finalized Release 17, the first version to treat satellites as a native part of the cellular network. It defined them as base stations, carved out new radio bands for satellite access, and wrote the Doppler and timing corrections into the rules so a chip could apply them automatically. Once that text existed, modem makers such as Qualcomm and MediaTek could all design to the same page.

The technology remains early. For now it is mostly text messaging, not calls or streaming; a message can take a minute to send, and a user may need a clear view of the open sky. Claims of full-speed "5G from space" describe a roadmap, not a shipping product. The hard part — making the link work at all — is finished; higher speeds are still to come.

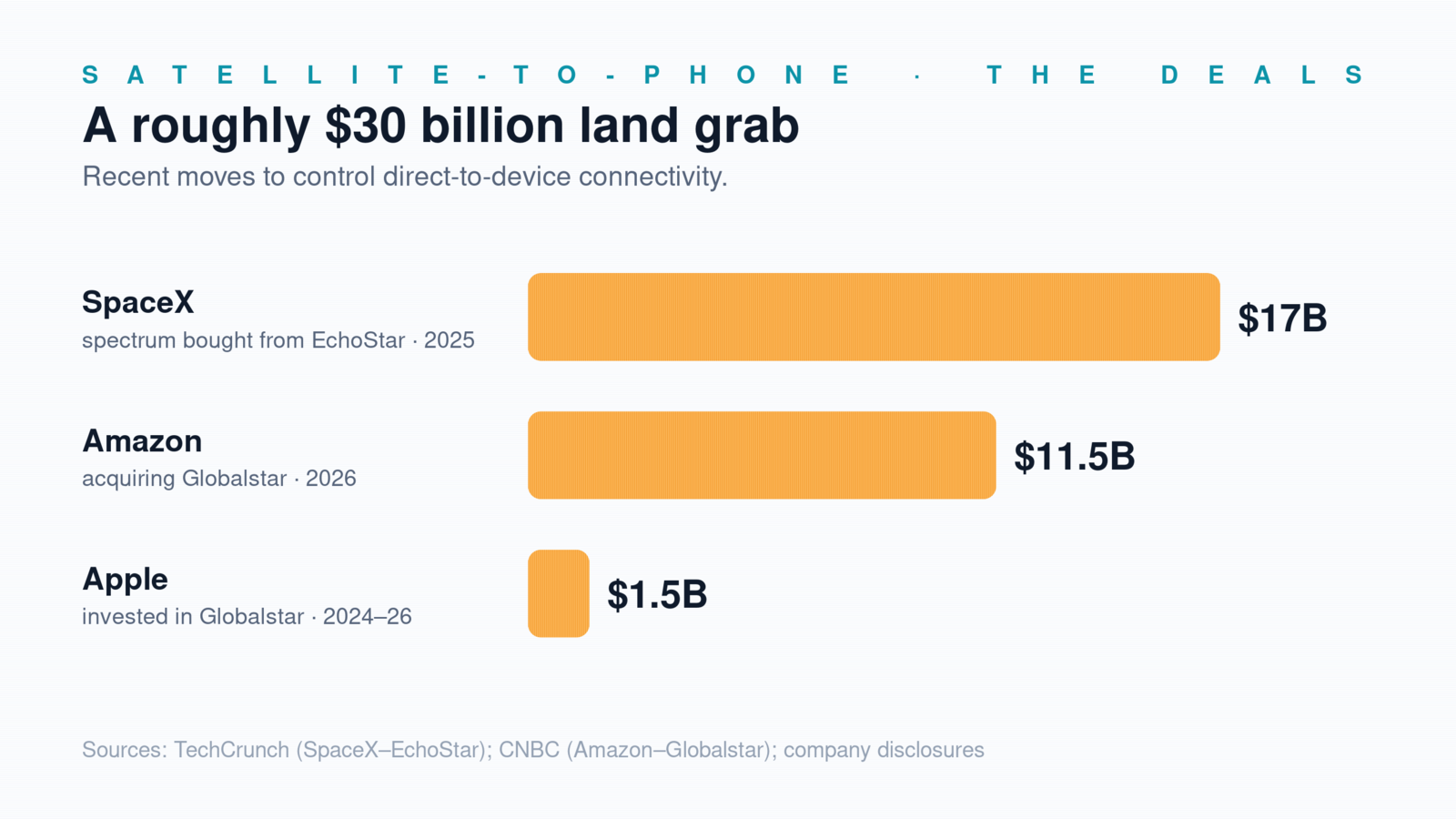

A $30 billion scramble for spectrum

With the physics largely settled, the contest has shifted to spectrum — the licensed frequencies these services depend on. In 2024, the FCC adopted the first framework of its kind, Supplemental Coverage from Space, allowing satellites to use mobile carriers' ground frequencies. That turned carrier spectrum into potential satellite spectrum, and the deals followed. In September 2025, SpaceX agreed to pay about $17 billion for the spectrum of EchoStar (NASDAQ: SATS) to feed Starlink's direct-to-phone service. In April 2026, Amazon (NASDAQ: AMZN) agreed to acquire Globalstar for roughly $11.5 billion (NYSE American: GSAT) — the same network behind Apple's satellite feature — as it builds a constellation to rival Starlink. Apple has separately invested about $1.5 billion in Globalstar.

The prize is large. Roughly 82 percent of the Earth's landmass has no cellular coverage, and about 2.9 billion people remain offline. The research firm Omdia projects direct-to-device service revenue will approach $12 billion by 2030.

What it means now

Much of this is already available to consumers. iPhones from the 14 onward include the feature in Settings, with a demo mode that helps locate a passing satellite without an emergency; T-Mobile, AT&T and Verizon phones may fall back to T-Satellite automatically when they lose signal. AST SpaceMobile expects dozens of satellites in orbit by the end of 2026, and T-Satellite is beginning to add data services. The dead zone is not gone. But for the first time it is shrinking — and the map's last blank spaces have become some of the most contested real estate in telecommunications.